Customised Cover

Competitive Premiums

Quote & Buy Online

Quick Claim Settlement

Quote Calculator

Home Building - Sum Insured

Home Contents - Sum Insured

OUR SERVICES

What We Cover

Fire & Special Perils

The Bharat Griha Raksha policy is a standardized and cost-effective home insurance policy.

Alternative Accomodation

This section covers rent for a defined period of time in case insured property is not fit to live.

Burglary & Theft

This section covers losses to the Home Building and Home Content on account of Burglary/Theft/Larceny.

Jewellery & Valuables

Coverage of theft and accidental loss or damage to the jewellery, curios, works of art, paintings and other valuables

About Us

Who We Are

Our Partners

INSIGHTS

Related Articles

- 04 February 2024

Claims Procedure for your Home Insurance

If You suffer a loss because of an Insured Event, You must make a claim for Your financial loss at

- 04 February 2024

RBI and IRDA Regulations for a Home Loan and Home Insurance

When applying for a home loan in India, there's often confusion regarding the necessity of home insurance. It's important to

- 03 February 2024

Immediate notice to authorities in case of a home insurance claim

As soon as any loss or damage occurs to the Insured Property, You must give immediate report to appropriate legal

- 03 February 2024

Steps to prevent loss or damage in case of a home insurance claim

a. You must take all reasonable steps to prevent further loss or damage to Your Home Building and Home Contents.

- 02 February 2024

Claim form for home insurance claim

You must submit your claim in the insurer claim form at the earliest opportunity, but within 30 days from the

- 01 February 2024

Establishing loss in case of a home insurance claim

You must prove that the Insured Event has occurred, and the extent of physical loss or damage You have suffered

- 30 January 2024

Hyderabad – Residential Real Estate Overview

Residential sales for Hyderabad continue to grow despite the state facing the highest consumer price inflation in the country during

- 30 January 2024

Claim procedure in case you have more than one home insurance policy

If You have more than one policy with Us or any other Insurance Company (taken by You or by anyone

- 29 January 2024

Chennai – Residential Real Estate Overview

The Chennai residential market has been on a recovery path since H2 2020. Sales increased by 3% YoY during H1

- 29 January 2024

India needs a national disaster pool to hedge natural disaster risks

India's vulnerability to natural disasters, including floods, cyclones, earthquakes, and droughts, is well-documented. These events not only result in loss

- 28 January 2024

Free look up period in home insurance

The free look-up period, also known as the free look period or free look provision, is a specific timeframe provided

- 28 January 2024

Impact of credit score on home insurance

Yes, credit score can impact your home insurance policy. We often use credit-based insurance scores as one of the factors

- 27 January 2024

Ahmedabad – Residential Real Estate Overview

Ahmedabad has historically been the most affordable market among the top eight cities under our coverage. This can largely be

- 27 January 2024

Impact of renovation on your home insurance

Renovating a home may increase the value of your home which could result in higher replacement costs in the event

- 26 January 2024

Bangalore – Residential Real Estate Overview

Bengaluru residential market continued to remain steady in H1 2023, despite facing multiple headwinds in the last one year arising

- 23 January 2024

Can you get insurance if the home is not used for housing purposes?

Yes, it is possible to obtain home insurance for a property that is not used for housing purposes . While

- 22 January 2024

What does the colour of your room say about you?

The colour of your room can provide insights into your personality and preferences. Different colours evoke different emotions and can

- 21 January 2024

Which way should the temple of your home face?

The direction in which a temple should face within a home can vary based on cultural and religious beliefs. In

- 20 January 2024

Delhi NCR – Residential Real Estate Overview

In H1 2023, the National Capital Region (NCR)’s primary residential market witnessed steadfast homebuying demand. However, the conspicuous annual growth

- 19 January 2024

What can you do if a financial institution forces you to buy a home insurance policy from them?

If your financial institution has internal guidelines that require mandatory home insurance to avail home loan benefits, it is not

- 17 January 2024

Kolkata – Residential Real Estate Overview

The residential real estate market in Kolkata continues to benefit from the 2% stamp duty rebate and the 10% rebate

- 16 January 2024

Home Building Cover under a standard home insurance policy

What is covered: The insurer will cover physical loss or damage, or destruction of Your Home Building because of any

- 16 January 2024

Insured events under a standard home insurance policy

We cover physical loss or damage, or destruction caused to the Insured Property by Fire (However, fire caused by burning

- 16 January 2024

Benefits of renewing your home insurance policy on time:

Here are some benefits of renewing your home insurance policy on time: Cost Savings: Renewing your house insurance on time

- 15 January 2024

What to do if a financial institution forces you to buy home insurance policy?

If your financial institution requires mandatory home insurance to avail home loan benefits but insists on purchasing insurance exclusively from

- 14 January 2024

Tips for finding the best home insurance online

Here are some important tips to consider when selecting the right home insurance plan: Compare Home Insurance Plans: Start by

- 13 January 2024

Mumbai – Residential Real Estate Overview

Mumbai continues to maintain its position as the largest market in terms of real estate sales with sales of 40,798

- 12 January 2024

Pune – Residential Real Estate Overview

In the first half of 2023, the residential market in Pune remained stable as it recorded total sales of 21,670

- 11 January 2024

Why should you buy Home Insurance

Home insurance protects your home building and home contents such as interiors, furniture, appliances, electronics & jewelry against fire, natural

- 11 January 2024

Significance of paintings in your home

Having paintings in your home can symbolise various things depending on the context and personal interpretation. Here are a few

- 10 January 2024

What are the risks covered under a home insurance policy?

Fire and Special Perils: Covers loss or physical damage due to fire, explosion or implosion, lightning, earthquake, volcanic

- 09 January 2024

Basis of valuation of home building under a home insurance policy

You can insure your home building on Reinstatement Cost Basis or Agreed Value Basis. Under reinstatement cost basis, your building

- 09 January 2024

Cost of a home insurance policy

It is more affordable to get home insurance than motor insurance A rough illustration – For a Home Building Sum

- 08 January 2024

What is the definition of home building under a home insurance policy?

Your Home Building is a building consisting of a residential unit, having an enclosed structure and a roof, basement (if

- 07 January 2024

Exclusions under a standard home insurance policy

The insurer does not cover losses and expenses for any loss or damage or destruction of the Insured Property that

- 07 January 2024

Optional covers under a standard home insurance policy

A standard home insurance policy or Bharat Griha Raksha (BGR) offers the following optional covers: (i) Cover for Valuable Contents

- 06 January 2024

What are some tips for finding the best home insurance policy for you?

Here are some crucial tips to consider when finding the right home insurance plan: Compare Home Insurance Plans: Begin the

- 05 January 2024

Key definitions in a standard home insurance policy in India

Carpet Area means: 1. for the main building unit of Your Home, it is the net usable floor area, excluding

- 03 January 2024

Home Insurance Applicability depending on Purpose of Home

Use for residence a. The insurer will pay only if Your Home Building is used for the purpose of residence

- 02 January 2024

Raising a Claim

To file a claim under a Home Insurance policy, you can follow these steps: Notify the insurance provider by calling

- 01 January 2024

Bharat Griha Raksha Policy

Bharat Griha Raksha is a comprehensive Standard Fire and Special Perils policy designed to safeguard against a wide array of

- 01 January 2024

Types of Home Insurance Coverage in India

Fire and Special Perils: Covers loss or physical damage due to fire, explosion or implosion, lightning, earthquake, volcanic eruption or

- 31 December 2023

Lower your home insurance premium

Here are some strategies to lower your home insurance costs: Share Repair Burden: Agreeing to share the repair costs can

- 31 December 2023

Eligibility to buy Home Insurance

Individuals meeting the following criteria are eligible to purchase a home insurance policy: The individual must be a resident of

- 30 December 2023

Who should buy home insurance?

A household insurance policy caters to individuals who reside in a home, whether they own or rent it. It's crucial

- 28 December 2023

Documents required to raise a home insurance claim

Here are the documents that need to be submitted along with the claim form to initiate a claim under the

- 27 December 2023

Handy tips for choosing a home insurance plan

When comparing different home insurance providers in India, it's essential to consider several key factors to ensure you make an

- 26 December 2023

Renewal of your home insurance policy

End of Policy: This Policy will expire at the end of the Policy Period. Renewal is not automatic, the Insurer

- 25 December 2023

Cancellation of your home insurance policy by you

You can cancel this Policy at anytime by giving the Insurer notice in writing. The Policy will terminate when the

- 24 December 2023

Cancellation of your home insurance policy by the Insurer

The Insurer will not cancel the Policy during the policy period except on the grounds of mis-representation, non-disclosure of material

- 23 December 2023

Automatic termination of your home insurance policy

Your Policy will automatically end in the following cases: Destruction of Your Home Building: This Policy will automatically end 7

- 22 December 2023

What happens in case of a fraudulent claim in home insurance?

If You, or anyone on Your behalf, make a false or fraudulent claim, or support a claim with any false

- 21 December 2023

What happens if you have more than one home insurance policy in case of a claim?

If You have more than one home insurance policy (taken by You or by anyone else for You) covering in

- 20 December 2023

Recovery action by insurer in case of a home insurance claim

When the Insurer accepts and pays Your claim under the Policy, the Insurer can start legal proceedings to recover the

- 19 December 2023

Changes to covers in your home insurance policy

You can choose to make changes to the covers of this Policy as may be permitted by the Insurer, or

- 18 December 2023

Waiver of Underinsurance in Home Insurance

A waiver of underinsurance in home insurance is an optional clause that can significantly impact how your claim is handled

- 17 December 2023

Nomination in home insurance

You can nominate a person to receive the claim amount under this Policy in the event of Your death. You

- 16 December 2023

Growing importance of home insurance

Home insurance has indeed become increasingly important in the face of rising natural calamities, global warming, and climate change. Here

- 15 December 2023

India lost $4bn to extreme weather in 2022

According to a recent report from the World Meteorological Organization (WMO), India experienced economic losses amounting to $4.2 billion in

- 14 December 2023

India lost $87bn in 2020 due to natural calamities

According to a report released by the World Meteorological Organization (WMO) on Tuesday, natural disasters like cyclones, floods, and droughts

- 13 December 2023

Uninsured losses of $32.94bn in India due to natural disasters in the last 5 years

Natural catastrophes in India resulted in uninsured economic losses totaling $32.94 billion (Rs 273,500 crore) during the five-year period from

- 12 December 2023

Cyclone Amphan impact | Insured losses may touch Rs 350 crore

Initial estimates suggest that insured losses resulting from Cyclone Amphan, which struck West Bengal and parts of Odisha on May

- 11 December 2023

Cyclone Amphan claims 133 lives and 15bn dollar loss

The report highlights the impact of Cyclone Amphan across India, Bangladesh, and Sri Lanka in May, resulting in the deaths

- 11 December 2023

Exclusions under a standard home insurance policy

The insurer does not cover losses and expenses for any loss or damage or destruction of the Insured Property that

- 10 December 2023

Indian Insurers need to buck up in climate sector related losses

According to a recent analysis of the global climate insurance sector, Indian insurance companies rank among the lowest performers worldwide

- 09 December 2023

West Bengal: Cyclone Amphan generated most claims for weather-related losses in 2020-21

The aftermath of Cyclone Amphan in May 2020 has propelled Bengal to the forefront of insurance claims for losses due

- 08 December 2023

Cyclone Michaung: Chennai’s image as an industrial hub has taken a hit

The feared business impact of Cyclone Michaung and the devastation it has caused in Chennai, India's fourth-largest city and a

- 07 December 2023

Heavy rains killed 44 in Telangana, caused Rs. 4,500Cr damage

The intense rainfall that caused widespread destruction across various regions of Telangana in two episodes from July 18 to 28

- 06 December 2023

How to choose IDV of your car for motor insurance?

The IDV represents the maximum sum insured amount that the insurance company will pay in case of total loss or

- 06 December 2023

Does Vastu Really Matter?

Vastu Shastra is indeed an ancient Indian architectural and design system that emphasizes harmony between humans and their environments. It

- 05 December 2023

What are the different add-ons available on a Own Damage or Comprehensive motor policy in India?

In India, insurance companies offer various add-on covers or riders that can be added to Own Damage or Comprehensive motor

- 04 December 2023

Benefits of Home Insurance

Home insurance, also known as property or homeowner insurance, offers protection for both the structure and belongings of a house

- 03 December 2023

Home Insurance Policy Tenure

Home insurance policies come in two types, differentiated by their tenure. Let’s delve into an explanation of each Simple or

- 02 December 2023

Vastu tips that you can consider for your home

Entrance Orientation: Ensure that the main entrance to your home faces east, north, or northeast direction. These directions are considered

- 01 December 2023

Importance of Vastu Shastra

Vastu for your home is important for several reasons: Harmony and Well-being: Vastu principles aim to create harmony between the

- 30 November 2023

What does Vastu Shastra say about the dining room of your home?

In Vastu Shastra, the dining room holds significance as it is where family members gather to eat and share meals,

- 29 November 2023

What does Vastu Shastra say about the bedroom of your home?

In Vastu Shastra, the bedroom holds significant importance as it is where individuals rejuvenate, rest, and replenish their energy. Here

- 28 November 2023

What does Vastu Shastra say about the kitchen of your home?

In Vastu Shastra, the kitchen is considered a crucial area of the home as it is where food, which sustains

- 27 November 2023

What does Vastu Shastra say about the temple/worshipping room of your home?

In Vastu Shastra, the temple or worshipping room, often referred to as the "puja room" or "mandir," holds special significance

- 26 November 2023

What does Vastu Shastra say about the entrance of your home?

In Vastu Shastra, the entrance of your home, also known as the main door or "entrance gate," is considered a

- 25 November 2023

What does Vastu Shastra say about the colours of your home?

In Vastu Shastra, colors play a significant role as they are believed to influence the energy flow within a home

- 24 November 2023

What does Vastu Shastra say about the living room of your home?

In Vastu Shastra, the living room holds significant importance as it is where family members gather, socialize, and entertain guests.

- 23 November 2023

Pointers to keep in mind before buying a motor insurance

Before buying motor insurance, there are several key pointers you should keep in mind to ensure you get the right

- 22 November 2023

What are the different types of motor insurance policies in India for private vehicles?

In India, there are primarily three types of motor insurance policies available for private vehicles, mandated by the Motor Vehicles

- 20 November 2023

Is motor insurance mandatory in India?

Yes, motor insurance is mandatory in India as per the Motor Vehicles Act, 1988. There are two main types of

- 19 November 2023

How to increase your NCB discount in motor insurance?

To increase the No Claim Bonus (NCB) in motor insurance, policyholders can follow several strategies and practices. NCB is a

- 18 November 2023

Pay As You Drive and Pay How You Drive Motor Insurance

Here's an overview of PAYD and PHYD insurance models: Pay As You Drive (PAYD): PAYD insurance bases premiums on the

- 18 November 2023

Importance of renewing your motor insurance policy on time

Renewing motor insurance on time is crucial for several reasons: Continuous Coverage: Renewing your motor insurance on time ensures that

- 17 November 2023

What do in case of a fire break out in your home building?

Experiencing a fire in your home building can be a frightening and dangerous situation. Here are steps to take in

- 16 November 2023

Handy tips when looking for a home loan

Availing a home loan for your dream home is a significant financial decision. Here are some tips to consider to

- 15 November 2023

Home Loan Insurance in India

In India, home loan insurance, also known as home loan protection plan or home loan insurance policy, is a type

- 11 February 2023

Personal Accident Cover under a standard home insurance policy

In the event an insured peril that caused damages to Your Home Building and/or Home Contents also results in the

- 11 February 2023

Cover for Valuable Contents under a standard home insurance policy

This is an optional cover under a standard home insurance policy Cover for Valuable Contents on Agreed Value Basis (under

- 11 February 2023

What the Insurer pays under Home Contents cover

If the General Contents of Your Home are physically damaged by any Insured Event, the Insurer will at their option,

- 11 February 2023

Restoration of Sum Insured of Home Contents Cover under a stand Home Insurance Policy

The insurance cover will at all times be maintained during the Policy Period to the full extent of the respective

- 11 February 2023

Sum Insured of Home Contents Cover under a stand Home Insurance Policy

The Sum Insured for the Home Contents Cover is shown in the Policy Schedule and will be the maximum amount

- 11 February 2023

Home Contents Cover under a standard Home Insurance Policy

The Insurer will cover the physical loss or damage to or destruction of the General Contents of Your Home caused

- 11 February 2023

Loss of Rent and Rent for Alternative Accomodation under a standard Home Insurance Policy

The Insurer will pay the amount of rent You lose or alternative rent You pay while Your Home Building is

- 11 February 2023

What the insurer pays under a standard home insurance policy?

If you make a claim under the policy for damage to Your Home Building due to any of the insured

- 11 February 2023

Restoration of Sum Insured of Home Building under a standard home insurance policy

Except as stated in your Policy, the insurance cover will at all times be maintained during the Policy Period to

- 11 February 2023

Sum Insured of Home Building under a standard home insurance policy

The Sum Insured for the Home Building Cover is the prevailing Cost of Construction of Your Home Building at the

TESTIMONIALS

See What Our

Customers Are Saying

Tarang Jhunjhunwala

Happy to have come across InsureMyHome. The team helped me get a thorough and complete understanding of why I needed a home insurance. Would definitely recommend to anyone who is a home-owner

Mr. Mudit Nahata

Mr. Gursahib Singh

WHAT? WHY? HOW?

Frequently Asked Questions

Home insurance protects your home building and home contents such as interiors, furniture, appliances, electronics & jewellery against fire, natural calamities, theft, burglary and 30 other risks. A home insurance policy provides peace of mind safeguarding you from any unforeseen financial costs

Home insurance covers the building structure of your home (including plinth and foundation) against unexpected loss or physical damage. Home insurance provides coverage for your own home, rented home, multi-storey apartment or private bungalow

You can also cover the contents of your home such as furniture, interiors, fixtures & fittings, household appliances, electronic gadgets, jewellery and valuables against unexpected loss or physical damage

Fire and Special Perils: Covers loss or physical damage due to fire, explosion or implosion, lightning, earthquake, volcanic eruption or other like convulsions of nature, storm, cyclone, typhoon, tempest, hurricane, tornado, tsunami, flood, inundation and 14 other risks.

Rent for Alternative Accomodation: Covers rent for a defined period of time in case the insured property is not fit to live. Some plans will cover the reasonable increase in living expenses within the same city in the event of the property getting damaged/destroyed on account of an accident during the policy period

Theft & Burglary: Covers loss or physical damage to your home contents due to theft and burglary

Jewellery & Valuables: Jewellery, precious stones, curios, antiques, Fine Arts, “Pair & Set” and items of similar nature is covered under this section. This section covers all risks of direct physical loss or damage to Valuable articles anywhere in India and worldwide (on a temporary basis)

Domestic Electrical & Electronic Appliances: This section includes items like AC, TV, Fridge, Oven, Music System and items of similar nature. This section covers loss or damage to the domestic electrical and electronic items from unforeseen and sudden mechanical and/or electronic breakdown

Portable Electronics: Covers loss or damage to portable electronic items like mobile phones, laptops, tablets, cameras, iPads etc. from unforeseen and sudden electrical breakdown

Baggage: Covers theft and accidental loss or damage to the personal baggage accompanying and belonging to you and/or your family on a trip undertaken outside the municipal limits of the insured city or while temporarily carrying anywhere in the world. Some plans also indemnify the expense incurred for contingency purpose occasioned by the loss

Public Liability: Covers damage on account of legal obligation and defence cost for personal injury or property damage caused to guests or a third party. This section offers coverage to the insured and his/her family members. Some plans may cover on a worldwide basis

Personal Accident: Covers death or disability of the insured or his/her family members or his/her domestic staff due to injury caused by an accident during the policy

Pet Cover: Covers your pet dog or pet cat against any unforeseeable event. This section indemnifies the veterinary expenses on account of road accident, poisoning, dacoity, robbery, terrorism, death of the pet and theft of the pet from home premises

A home insurance policy can be taken for 1 year, 3 years, 5 years or 10 years

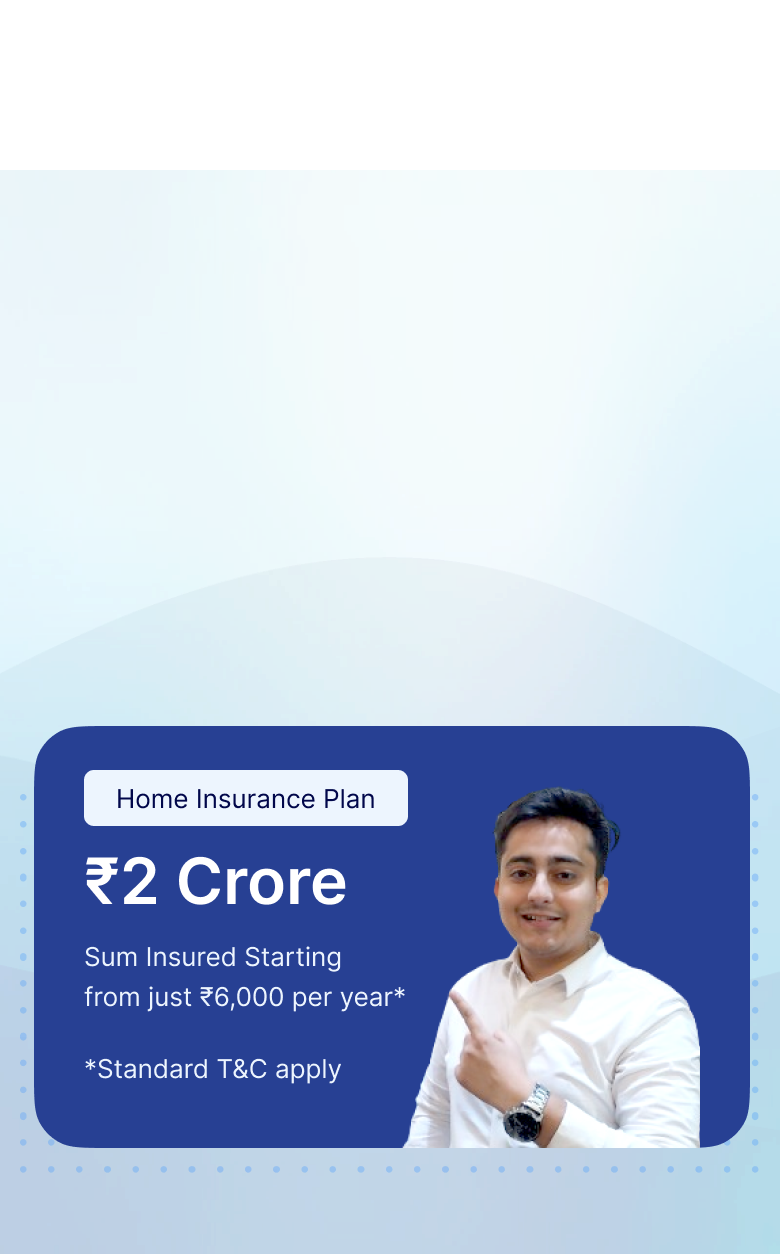

A rough illustration – For a Home Building Sum Insured of Rs. 2Cr and Home Contents Sum Insured of Rs. 20 Lacs against Fire & Special Perils and Theft & Burglary, annual premium would be approximately Rs. 6,500/- – Rs. 7,000/-

Actual costs may vary depending on coverages, product and insurer

You can insure your home building on Reinstatement Cost Basis or Agreed Value Basis. Under reinstatement cost basis, your building sum insured is equal to Carpet Area multiplied by Present Day Cost of Reconstruction based on your local area/municipality. In case of a claim, the insurer will pay you the cost of reconstructing/repairing your home building to a state similar to the condition before the accident

Under Agreed Value Basis, you can insure your home building on market value. A valuation report by a government approved valuer would be required in case of a claim. In case of a claim, the insurer will pay you the Sum Insured only if you choose not to or are unable to reconstruct/repair your home building

Your Home Building is a building consisting of a residential unit, having an enclosed structure and a roof, basement (if any) and used as a dwelling place

Your Home Building includes

(i) fixtures and fittings permanently attached to the floor, walls or roof, like fixed sanitary fittings, electrical wiring and other permanent fittings

(ii) the following ‘additional structures’ if they are on the same site and used as part of your Home Building:

Garage, domestic outhouses used for residence, parking spaces or areas, if any

Compound walls, fences, gates, retaining walls and internal roads

Verandah or porch and the like

Septic tanks, bio-gas plants, fixed water storage units or tanks

Solar panels, wind turbines and air conditioning systems, central heating systems and the like, if not included in Home Contents cover

(iii) Any other structure shown in the Policy Schedule

Your Home Building does not include Contents of Your Home

A standard home insurance policy or Bharat Griha Raksha (BGR) offers the following optional covers:

(i) Cover for Valuable Contents on Agreed Value Basis (under Home Contents Cover):

For Valuable Contents, a value may be agreed upon by You and Insurer based on a valuation certificate submitted by You and accepted by Insurer. However, the insurer may waive the requirement of a valuation certificate if the Sum Insured opted for is up to Rs. 5 Lacs and individual item value does not exceed Rs. 1 Lac. If the Valuable Contents of your Home are physically damaged by any Insured Event, insurer will pay the cost of repairing the items. If the Valuable Contents of your Home are a Total Loss, insurer will pay the Sum Insured shown in the Policy Schedule for the Valuable items.

(ii) Personal Accident Cover

In the event an insured peril that caused damages to your Home Building and/or Home Contents also results in the unfortunate death of either You or Your Spouse, the insurer will pay a compensation of Rs. 5 lacs per person

In the event of the unfortunate death of the Insured, the Personal Accident cover shall continue for the Spouse until expiry of the Policy

The insurer does not cover losses and expenses for any loss or damage or destruction of the Insured Property that is directly or indirectly as a result of or is caused by or arising from events, stated below:

A) Your deliberate, wilful or intentional act or omission, or of anyone on your behalf or with your connivance

B) War, invasion, act of foreign enemy hostilities or war-like operations (whether war is declared or not), civil war, mutiny, civil commotion amounting to a popular rising, military rising, rebellion, revolution, insurrection or military or usurped power

C) Ionising radiation or contamination by radioactivity from any nuclear fuel or from any nuclear waste from combustion of nuclear fuel or the radioactive, toxic, explosive or other hazardous properties of any explosive nuclear assembly or nuclear component that is part of it

D) Pollution or contamination, unless (i) the pollution or contamination has itself resulted from an Insured Event or (ii) an Insured Event itself results from pollution or contamination

E) Loss, damage or destruction to any electrical/electronic machine, apparatus, fixture, or fitting by over-running, excessive pressure, short circuiting, arcing, self-heating or leakage from electricity from whatever cause (Lightning included). This exclusion applies only to the particular machine so lost, damaged or destroyed

F) Loss or damage to bullion or unset precious stones, manuscripts, plans, drawings, securities, obligations or documents of any kind, coins or paper money, cheques, vehicles, and explosive substances unless otherwise expressly stated in the Policy

G) Loss of any Insured Property which is missing or has been mislaid, or its disappearance cannot be linked to any single identifiable event

H) Loss or damage to any Insured Property removed from your Home to any other place

I) Loss of earnings, loss by delay, loss of market or other consequential or indirect loss or damage of any kind or description whatsoever

J) Any reduction in market value of any Insured Property after its repair or reinstatement

K) Any addition, extension, or alteration to any structure of your Home Building that increases its Carpet Area by more than 10% of the Carpet Area existing at the Commencement Date of or on the date of renewal of this Policy, unless you have paid additional Premium and such addition, extension or alteration is added by Endorsement

L) Costs, fees or expenses for preparing any claim

Immediately notify the insurer about the claim. Once the First Information Report (FIR) is filed, and the insurance provider is informed, the policyholder should furnish all pertinent and relevant information concerning the purchased policy and the incurred damage. Upon receiving the claim request, the insurer starts the process of validation and verification. Following this, the claim settlement request is forwarded to the claims department of the specific insurance company. Within the next 48 hours or so, a surveyor is dispatched to assess the damage or loss and subsequently prepares a report. All additional necessary documents are to be submitted to the surveyor. The surveyor then prepares the Final Survey report, which, along with the required documents, is submitted to the insurance provider within 7 days.

If your financial institution has internal guidelines that require mandatory home insurance to avail home loan benefits, it is not compulsory to purchase insurance coverage from them. However, if your bank insists on buying home insurance exclusively from them, consider the following steps:

Compare Policies: Compare home insurance quotes offered by financial institutions with those from other insurers.

Evaluate Premiums: If the difference is minimal, it may be convenient to opt for the financial institution’s offerings in this case.

Refuse if Overpriced: If the lender’s home insurance premium is significantly higher than other insurers in the market, it is wise to decline their proposal. Additionally, consider other factors such as customer assistance facility, additional services, claim settlement process, etc.

Raise a Complaint: If the financial institution remains uncooperative, file a complaint with the manager

Consider Another One: If all else fails, explore other financial institutions that will cooperate with you for your home loan needs.

Here are some crucial tips to consider when finding the right home insurance plan:

Compare Home Insurance Plans: Begin the home insurance buying process by visiting InsureMyHome.co.in

Compare home insurance quotes from reputable insurance companies in India based on your requirements.

Know Your Coverage Needs: Examine what aspects of your property you want to cover, such as the structure and its contents. For instance, if you are a tenant, buy only content cover and skip building structure coverage.

Know the Financial Strength of the Insurer: Check the financial stability of the shortlisted insurers and their claim settlement ratio to get a fair idea of how the company operates.

Check Customer Reviews: Read customer reviews on the insurer’s website and related social media platforms for better insights into their service quality and customer experiences. Choose an insurer and a policy that aligns with your requirements and budget.

Choose the Right Sum Insured: Calculate the appropriate sum insured based on your property’s size and the value of your belongings. Additionally, take advantage of add-ons for extended coverage at the most nominal premium.

Home insurance policies come in two types, differentiated by their tenure. Let’s delve into an explanation of each

Simple or Short term policies:

These policies provide coverage for the home and its associated contents for a tenure ranging from one to three years. They offer comprehensive protection for your house structure, safeguarding against risks such as theft, damage, loss of personal belongings, accidental loss, and fire outbreaks. Despite having a shorter tenure, these policies are relatively more affordable compared to long-term options.

Long term policies:

True to their name, these policies are crafted for extended coverage, spanning up to 30 years. They provide comprehensive protection against all major risks. Additionally, you have the option to enhance coverage by purchasing add-on covers for an extra premium. Given the longer tenure, the associated risks increase, making these policies relatively more expensive than their simpler counterparts.

Here are some benefits of renewing your home insurance policy on time:

- Cost Savings: Renewing your house insurance on time can result in significant savings. If you let it expire, purchasing a new policy can be a more expensive undertaking

- Enhanced Property Value for Buyers: While home insurance plans aren’t transferable, renewing your policy reflects responsibility to potential buyers. They perceive you as a conscientious seller, contributing to the assurance that the home is well-protected

- Updated Property and Contents Valuation: Timely renewal keeps you informed about your home and its contents’ current value. The renewal process often involves a revision of valuation metrics, assisting you in understanding the current market value, which can be beneficial when planning to sell your house.

- Long-term Security for Future Generations: Your home is a lifetime investment. Timely renewal ensures that your property is well-maintained and protected from various risks, providing long-term security for future generations. Owning a secure house becomes a valuable asset for your descendants.

Renewing your home insurance policy on time not only brings financial benefits but also establishes a sense of responsibility and foresight, securing both your present and your legacy.